Part III of Understanding Your NH Workers’ Compensation Premium

The relationship between what you pay your employees, and what you pay in premium.

Review

In the third and final installment of this series we’re talking about payroll. This will conclude our review of the key cost-driving factors, and explain how payroll is used in the formulation of your workers’ compensation premium. To cap everything off, we’ll practice what we’ve discussed by walking you through a premium estimate for a mock business.

We now know that class codes are used across the insurance industry to categorize different jobs by the risk of the work performed by employees. Since workers compensation covers work related injuries incurred by your staff, your premium needs to account for the likelihood of injury, or the amount of risk. Class codes are factored into your premium calculation to do just that.

We’ve also covered how a business gets their experience modification number, and how to keep your workers compensation positioned for preferential rating.

Now, we are onto payroll.

Step 1 – Breaking down payroll by class code.

Many of you have a good grasp on how payroll works. To get an accurate workers compensation quote or to correctly setup your policy, providers need your annual payroll to be broken into earnings by class code. A good agent will take the time to discuss accurate classifications with a carrier, and make sure your policy reflects the different jobs performed by your employees.

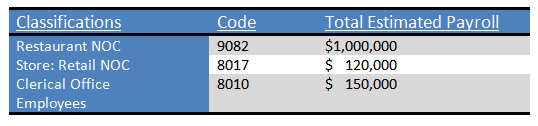

In the restaurant industry the entire payroll could fall under one class code. This is relatively common, but not always the case. Let’s say that in addition to your service staff your restaurant has a retail store or gift shop and a dedicated full-time admin department. In this situation we could have payrolls for 3 distinct class codes. To give you an idea of what that might look like, see the example below for The Fake Falafel Diner:

Payroll Breakdown for The Fake Falafel Diner

Step 2 – Factor In Your Experience Modification Factor

Let’s assume The Fake Falafel has a friendly Experience Modification Factor of .88 due to their ongoing workplace safety efforts. The experience mod is the final piece of information needed to estimate the workers compensation premium paid by The Fake Falafel Diner.

Step 3 – Input information and calculate estimate.

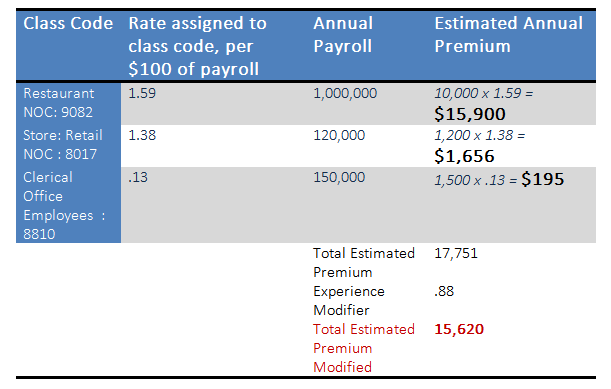

Using a table like the one below, insert the workers compensation factors that we have discussed. From left to right, multiply the class code rate by your payroll. Then add the cost for each class code together. Multiply the sum by your experience modification factor, and there you have it!

In other words…

Premium Estimate Example

The Fake Falafel Diner

But not so fast! Every insurance carrier has some flexibility in determining their rates. They may manipulate the calculation slightly for certain types of risks based on how comfortable and equipped they are to handle it. Different carriers also allow the use of multipliers and discounts for certain types of businesses. That is to say, the carriers your insurance agent has access to and their knowledge of the competitive markets for your industry is a big factor in how favorable your annual pricing ultimately ends up.

If you haven’t had a chance to read the first two articles you can find the entire series on our blog, Inside Insurance. This portion of our site delves into helpful tips and information about the topics that NH Business owners face. We provide concise and interesting insight on preparation, prevention and management. Please use our blog to gain clarity, while understanding that there is no “one size fits all” answer when it comes to protecting your business. We ask that you use your best judgement when considering how appropriate a particular tip is for you.

If you are seeking help for a specific circumstance, the best solution will always come from working one on one with an agent.

Questions about your NH Workers Compensation? Looking for a quote? We’re here to help NH businesses like you, navigate these often murky waters.